Toto Wolff, Mercedes-AMG Petronas F1 Team’s CEO and Head of Mercedes-Benz Motorsport, grew up with almost nothing in one of Europe’s wealthiest cities. He turned that dissonance into the most dominant team in Formula 1 history. And a personal fortune to match.

In A Farewell to Arms, Hemingway writes: “The world breaks everyone, and afterward, many are stronger at the broken places.” The story of Torger Christian Wolff, known universally as Toto, does not begin with privilege, with a famous father, or with a clear-cut path to the top. It begins in Vienna, Austria, in 1972, with a family coming apart at the seams, and a little boy learning about financial insecurity and profound loss.

Many people who grew up in situations of scarcity say that those memories never leave them. So if we want to understand why Toto Wolff is the way he is (meticulous, relentless, incapable of accepting mediocrity), we have to start there, in that city, under those circumstances.

The French School

Vienna wears its wealth openly with grand boulevards, the opera house, and the fancy boutiques. Growing up there, broke but surrounded by it, is an education in and of itself.

Wolff was born to a Polish mother and a Romanian father. His mother was a physician. His father was an entrepreneur who was diagnosed with brain cancer when Toto was a young child. His parents separated. His father deteriorated slowly, across a decade, until he died when Toto was just fifteen. That’s ten years of what Wolff has described as the “gradual dissolution of security”, the kind a kid depends on so that they can focus on just being a kid.

In his own words: “He was terminally ill for ten years, so basically all throughout my childhood. And (our) financial hardship was related to this.”

Despite the circumstances, his mother did something remarkable. She kept him enrolled at the Lycée Français de Vienne, one of Vienna’s most prestigious private schools. That single decision gave Wolff his multilingual foundation and placed him inside a social network he could observe but not quite inhabit. He has recounted the story of him and his sister being pulled out of class in front of all their peers and sent home because their school fees hadn’t been paid. He was only fourteen years old. The memory of the humiliation he felt that day has never faded.

“I went to school in an affluent environment without being a part of it,” he told The Times. He would later reflect that the result was a specific type of hunger: not envy, exactly, but a refusal to accept the distance between what he could see in front of him and what he didn’t have.

He describes his school performance as “getting by with the smallest possible margin”. He passed his Matura (the Austrian school-graduating examination) at eighteen, which, given what was happening at home, he has called genuinely surprising.

He received two invaluable gifts from this school. The French he learned would prove useful for the rest of his life. And at seventeen, a friend invited him to watch a race at the Nürburgring in Germany. Something switched on inside him that day, and it never switched back off.

The Self-Aware Racer

What happened next is important to his story because of what it teaches us about Wolff’s brand of self-awareness.

He started racing and was quite serious about it. He competed in Austrian and German Formula Ford from 1992 to 1994. He won his category at the legendary Nürburgring 24 Hours in 1994. He loved every minute of it, but by the mid-nineties, he began to run out of money to fund his racing and, more importantly, to assess his ability. He was good. He was not elite.

This is actually a harder conclusion to reach than it may seem. People who get as far as Formula Ford are not hobbyists. They are competitive, committed, and have invested enormous time and self-belief in the idea that they belong in racing. Admitting, at 25, that your path runs through the paddock but not through the cockpit requires an immense amount of intellectual honesty.

Wolff pulled back from full-time racing. He enrolled at the Vienna University of Economics and Business, then dropped out. He hated the curriculum and wanted urgently to be dealing with real-world capital. He picked up an internship at an investment bank in Poland. “I went into an internship in a bank in Warsaw (my mother’s Polish), and I remember it was so bad.”

He stayed there long enough to absorb what he needed.

He then took a sales management role at Koloman Handler, an Austrian metal parts manufacturer founded in 1900 that became the largest producer of ring binder mechanisms in Europe, processing more than 5,000 tons of wire and steel annually. Not glamorous. But something important happened inside that company.

As Wolff has put it: “In 1996, I decided I wanted to be an entrepreneur. Koloman had taught me how to calculate margins as a percentage of the selling price, and within a year, I started analyzing how much the owner was going to make. I saw that I could earn more as a shareholder in the first year than as an employee.”

That was the moment. Not a dramatic epiphany, just a young man doing the math and deciding he was on the wrong side of the numbers. He began traveling to the United States, where the internet was beginning to take visible shape: Netscape, America Online, and mobile portals offering free SMS access. He came back to Vienna with one clear thesis: Everything he’d seen would exist in Austria too, and someone was going to profit from being early. He wanted to be that someone.

He scraped together enough money to fund consultancy stakes in early-stage technology companies. And then, in 1998, he made his first real move. He co-founded Marchfifteen.

The Internet, Cold Calls, and the First Real Money

The late 1990s were the kind of moment in European tech that will not be repeated. It was an era of genuine naivety where companies with no revenue could be acquired for extraordinary sums if someone believed hard enough in the underlying trend.

Wolff started cold-calling tech founders. He had almost no cash to offer. So the pitch was something else entirely: I will find you investors, help you structure the business, and get you listed. In exchange, all I want is equity.

Those early cold calls produced two landmark exits, both in the same year. The first was UCP, an Austrian text message software provider that Marchfifteen had backed in the early days of mobile communications. In 2006, UCP was acquired by Amdocs, a global technology company specializing in software for communications and media companies, for $275 million. The second exit that same year was Sysis, a mobile communications software company that Marchfifteen had taken public on the stock exchange in 2000, and which was subsequently sold to VeriSign. Between the two transactions, Wolff is reported to have netted approximately $30 million. For a man who had started with almost nothing, that number changed everything.

By 2004, he had founded a second firm, Marchsixteen, and expanded the strategy to medium-sized industrial companies and listed equities. The portfolio was methodical, patient, and built around the same logic he would bring to every subsequent decision: find the thing that is structurally undervalued, get in early, and have the discipline to wait.

The Bridge

By 2006, Wolff had begun looking for a place where his investment framework and his old racing passion could intersect. He found it in HWA AG, a German company that was basically the engineering backbone of Mercedes-Benz’s motorsport ambitions. HWA developed Mercedes’ Formula 3 engines and ran the brand’s DTM program.

HWA AG looked, on the surface, like a conventional German engineering company. Its entire purpose and value, though, was tied to motorsport. Wolff bought a 49% stake.

The following year, he listed HWA on the Frankfurt Stock Exchange. It was the same playbook: identify an underappreciated asset, take a substantial position, and create a liquidity event that realized the value others hadn’t seen. He divested his HWA stake in 2015. It had served its purpose.

The most important thing HWA gave him was visibility inside the Mercedes-Benz motorsport ecosystem. He had crossed from outside observer to insider, embedded in the architecture of how a major manufacturer approached racing. That proximity became the foundation for everything that followed.

In 2002, alongside F1 world champion Mika Häkkinen, Wolff co-founded a racing driver management company. Among the young drivers they backed were Finnish driver Valtteri Bottas, who would eventually race for him at the Mercedes-AMG Petronas F1 team, and Canadian Bruno Spengler, who would become DTM champion in 2012.

“In a way, I tried to give back to young drivers what I was missing: financing and advice.”

The young man who had been priced out of racing was now the man writing the checks for others trying to get in. Between that venture, HWA, and the Marchfifteen/Marchsixteen portfolio, a pattern was becoming clear: he was constructing a network aimed at one specific destination. Emphasis on the one.

Enter Williams

In 2009, the late Sir Frank Williams reached out to Toto directly because the Williams F1 team he founded in 1977, which had experienced so much glory in its heyday, had fallen on hard times. Wolff bought a 16.3% stake in Williams F1 and joined the board of directors as the only outside owner. By 2012, he was the team’s executive director. That same year, on a warm afternoon in Barcelona, Pastor Maldonado took the checkered flag for Williams’ first race win in nearly eight years.

It is also their last win as of the publication date.

Wolff arranged Williams’ IPO on the Frankfurt Stock Exchange in 2011, listing 27.39% of the company’s shares. The float valued the team at approximately $361.3 million. He was building the team's institutional infrastructure even as he managed it daily.

From across the paddock, the Mercedes factory team, which had returned to F1 in 2010 and was struggling to compete with the customer teams they were supplying, took notice.

What happened next remains one of the more quietly significant career moves in the sport’s modern history.

Mercedes asked Wolff to conduct an assessment of their F1 operation. They asked him to identify, from the outside, what was going wrong. He did. And then they asked him to come fix it. Wolff hesitated. He had a stake in Williams, so helping their engine supplier become a genuine competitor felt awkward, to say the least. Mercedes removed the hesitation, the only way that works with a man like him: they offered him equity.

The $58.5 Million Bet

In January 2013, Toto Wolff left Williams and joined Mercedes as executive director, team principal, and CEO. He acquired 30% of Mercedes-Benz Grand Prix Ltd (the holding entity for the F1 team), reportedly for around $58.5 million. Niki Lauda held another 10%. Daimler held 60%.

The 2014 season began, and Mercedes dominated in a way that nobody could have predicted. The new turbo-hybrid regulations suited the power unit Mercedes had been developing, and something about the Wolff-led team culture had fundamentally shifted the organization’s internal cohesion. Lewis Hamilton and Nico Rosberg crossed the line first, again and again and again.

What followed became the most dominant era in Formula 1 history.

Eight consecutive Constructors’ Championships, from 2014 to 2021. Seven consecutive Drivers’ Championships. Records that had stood for decades, toppled, one by one. More than half of all races run during that period were won by a single team. They didn’t just overtake the previous benchmark (Ferrari’s six consecutive Constructors’ from 1999 to 2004 and five consecutive doubles with Michael Schumacher at the helm), they lapped it.

During this run, the ownership structure evolved. When INEOS, the British chemical conglomerate controlled by Sir Jim Ratcliffe, bought into the team in 2020, Wolff’s stake increased to an equal one-third alongside Mercedes-Benz and INEOS, each holding 33%.

The team, acquired by its parent company for roughly $140 million in 2010, was valued at $6 billion by 2025.

Let’s do the math on what that means for the man who bought his stake at $58.5 million. His third of the team is now worth approximately $2 billion. He has since sold 15% of his holding company (the vehicle through which he owns his Mercedes shares) to CrowdStrike founder George Kurtz for $300 million. That transaction, announced at the 2025 Las Vegas Grand Prix, valued the team at a record $6 billion, surpassing McLaren's $4.7 billion stake sale just weeks earlier. Wolff remains as CEO and team principal, with roughly 28% of the team still in his possession.

The Paddock and the Professor

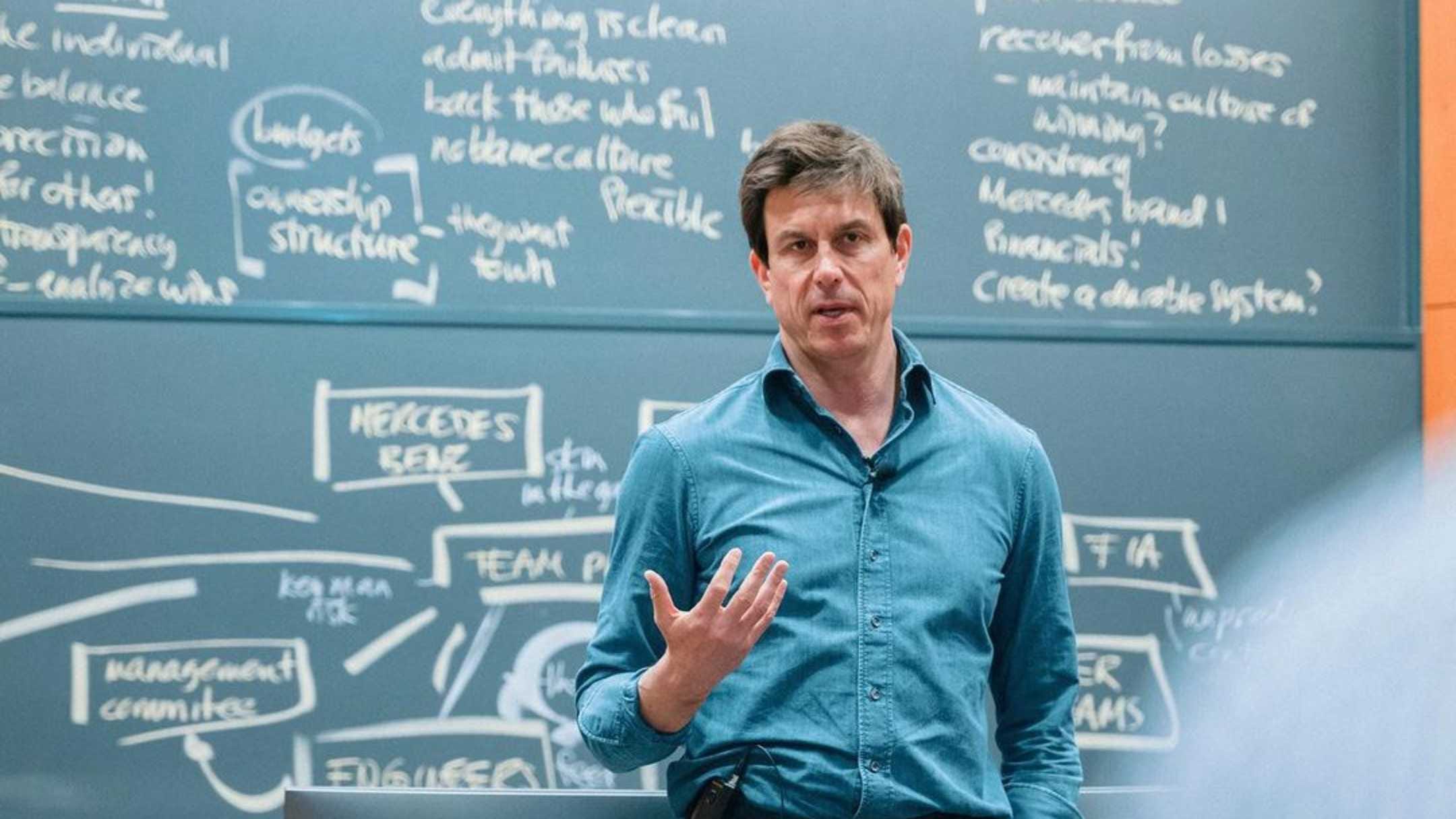

His success at Mercedes has produced something unusual: a team boss who has become an object of academic study. In 2022, Harvard Business School published a case study titled Toto Wolff and the Mercedes Formula One Team, authored by Professor Anita Elberse, who had spent time inside the operation studying how it maintained its culture under sustained competitive pressure. Wolff now co-teaches the case to MBA students as an Executive Fellow at Harvard Business School.

The Harvard connection reflects something real about what Wolff built at Brackley. The Mercedes operation during the dominant era was an organizational machine that generated alignment between engineers, strategists, drivers, and management, with a consistency that most corporations, let alone racing teams, cannot sustain across a single season, much less eight consecutive ones.

Wolff has spoken about what this costs personally. He has been candid about mental health, about the toll of high-performance environments, about the way the childhood fear of instability can masquerade as professional motivation until you are honest enough with yourself to separate the two. He has said that what happened in his early life left permanent scars. “I still wake up having dreamt I am alone,” he told The Daily Mail in 2021. “It’s a dream I have had since I was a child.”

Trophies don’t resolve trauma.

Behind the Dynasty

Here’s the financial architecture of the house that Toto built:

The Mercedes Valuation. At a $6 billion team valuation, set by the Kurtz transaction in November 2025, Mercedes recorded the highest transaction-verified valuation in Formula 1 history. For context, INEOS paid approximately $266 million for its equal third in 2020. Five years later, the same-sized stake would cost more than $2 billion. The revenue tells the same story: Mercedes posted approximately $813 million in revenue in 2024, the highest of any team on the grid, with a pre-tax operating profit of approximately $205 million and a net profit after tax of approximately $154 million, the first Formula 1 team in history to record a nine-figure net profit. The team declared a total dividend of approximately $160 million for 2024, with each of its three equal shareholders receiving approximately $53 million.

Wolff’s personal compensation. In 2024, Wolff’s total earnings from his Mercedes position exceeded $64 million. His base salary as team principal was approximately $7.7 million (confirmed in the Companies House filing), down from approximately $10.2 million the prior year. The far larger number came from dividends: Mercedes distributed approximately $171 million to its three equal owners across two tranches in 2024, meaning Wolff’s dividend income alone was approximately $57 million. His salary, in other words, is almost a footnote. The real money flows from ownership, which has been the logic of his entire career.

The Kurtz sale. In November 2025, Wolff sold 15% of his holding company, representing 5% of the team outright, to CrowdStrike co-founder and CEO George Kurtz for approximately $300 million. The logic was straightforward: Kurtz is a tech entrepreneur and an accomplished endurance racer in his own right. He has class victories at Le Mans, Spa, Sebring, and Road Atlanta. He’s a two-time Asian Le Mans LMP2 champion. And in January 2026, he finally claimed the one race that had eluded him: the Rolex 24 at Daytona.

Given how much of modern F1 is tied to data infrastructure and the American market, Wolff was explicit that Kurtz was chosen for what he brings, not merely what he paid.

Net worth. As of March 2026, Forbes’ real-time billionaires tracker ranks him 1,548th with a net worth of $2.7 billion. The largest single component is his Mercedes stake: before the Kurtz transaction, his 33% holding at the $6 billion valuation was worth approximately $1.98 billion; after selling 15% of his holding company to Kurtz, his remaining 28.33% stake is worth approximately $1.7 billion.

His portfolio extends beyond Mercedes. He holds a 0.95% stake in Aston Martin Lagonda, the British sports car manufacturer, acquired in April 2020 and subsequently diluted from an initial 4.95% position following a rights issue. He also has his ongoing Marchfifteen and Marchsixteen holdings, among other strategic positions. His annual compensation from Mercedes alone (salary plus performance bonuses) is confirmed at between $20 million and $26 million.

One More Rival. One More Room.

By March 2026, when the new Formula 1 season opened in Melbourne, we got a first look at where the Mercedes camp's attention might be pointed next.

The target: a 24% stake in Alpine F1, currently held by Otro Capital, an American private equity firm whose celebrity investors include golfer Rory McIlroy, actors Ryan Reynolds and Rob McElhenney (through their Maximum Effort Investments vehicle, the same partnership behind Wrexham AFC), NFL stars Patrick Mahomes and Travis Kelce, and Real Madrid star Trent Alexander-Arnold…among many others.

Otro paid approximately $233 million for the stake in 2023, and Alpine’s value has more than doubled since then, reaching approximately $3 billion. The 24% slice is now worth in the region of $750 million. More than three times what Otro originally paid.

Alpine’s polarizing executive advisor, Flavio Briatore, acknowledged that any minority shareholder would effectively be a “passenger” in Alpine’s decision-making. “Normally one company with 75% decides, and the 25% is a passenger, and this is the reality.”

So what could the strategy be behind acquiring a minority stake? The first conclusion is purely financial: given the upward trend in Formula 1 team valuations, a minority stake in Alpine is simply a strong investment. The second is strategic: Mercedes already supplies Alpine’s power units and gearboxes through at least 2030, and having equity in a customer team secures that relationship. The third is operational: with two teams running closely related mechanical packages, Mercedes gains access to a significantly larger volume of comparative development data. In theory, a closer relationship with Alpine could also create a pathway to evaluate young Mercedes drivers under real-racing conditions, something it currently lacks a direct mechanism for.

The complication, and the part of the story that has sent the paddock into a frenzy, is who else wants the same slice.

A man who publicly said at a Dublin event in January that he has “unfinished business” in Formula 1 and that he will only return as a partner, not a hired hand. Briatore confirmed there are “three or four potential buyers” for the Otro stake, with Horner among the interested parties.

Briatore was explicit on Friday at the Chinese Grand Prix: “I know there is a negotiation from Mercedes, not with Toto, with Mercedes, and we see.” Alpine has declined to comment on specific bidders. A Mercedes spokesperson said only: “Mercedes is a key strategic partner of Alpine, and we are being kept apprised of the latest developments.”

If Mercedes’ bid succeeds, Horner’s route back into F1 via Alpine is likely closed. Their on-track rivalry (the 2021 championship fight, the radio wars, the Abu Dhabi denouement) was the defining sporting conflict of the hybrid era.

Their relationship has apparently softened. Horner revealed on the recent season of Drive to Survive that Wolff sent him a text after his Red Bull sacking. But warm texts and competing for the same equity stake are completely different ball games.

The pattern is unmistakable. Williams in 2009. Mercedes in 2013. And now, thirteen years into the most dominant run in the sport’s history, Wolff and the institution he built are looking at the chessboard and figuring out which square to occupy next. The boy from Vienna has never been content to simply hold station. He is always planning his next move.

What Trauma Builds

There is a theory of performance, one you hear in elite sport and high-stakes finance and from highly successful individuals across every walk of life, that motivation doesn’t always come from ambition, but rather from a refusal to return to a state of powerlessness previously experienced.

Wolff has been direct about the connection between his childhood and his drive. “I think overcoming drama, trauma, and humiliation creates more motivation to prove that you’re worthy,” he told The High Performance Podcast. “I see that with many successful people. There was some kind of event, or situations that scarred them and caused pain.” The school fees. The tram ride home with his sister, trying to explain why they had been sent away. “It was quite a humiliating experience,” he said. “I wanted to make a better life for myself and did what I could to succeed.”

What he has been less public about, until recently, is that he has struggled significantly with his mental health throughout his adult life, and that he has sought help. He has been seeing a psychiatrist since 2004 and estimates he has accumulated more than 500 hours of therapy. “I have suffered mentally, and I still do,” he told the Sunday Times. “Getting help is a way of overcoming my problems, and it has helped me to access untapped potential.”

For a man who built an empire on control and precision, it’s a disarmingly candid admission. And it reframes the closing chapters of his story considerably: the championships, the billions, the Harvard fellowship. None of it resolved what lies beneath. It just gave him better tools to deal with it.

From Vienna to Harvard, by way of Brackley. For the boy sitting in that classroom in 1987, it would have seemed an unimaginable life.

But it turned out to be his.

Incredible read, thank you for this!

An amazing story